By Tony Petosa, Nick Bertino, and Matthew Herskowitz

When considering how to summarize our current economic and market conditions, we were reminded of an old idiom: we just can’t see the forest for the trees. In today’s world of fast-moving, multi-faceted media, we are so inundated by details and, in many cases, conflicting information that we fail to understand the big picture: It’s all part of a cycle!

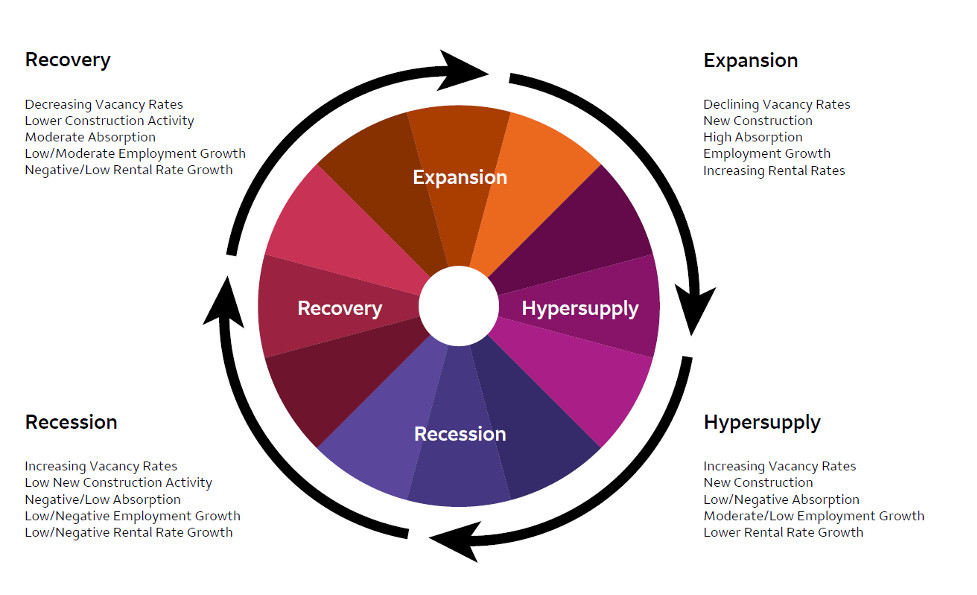

Taking a step back, it is helpful to recognize that there are four phases to a real estate cycle as outlined in the adjacent diagram: expansion, hyper-supply, recession, and recovery. While each cycle is unique and there are differences in how certain markets and properties perform, all cycles follow a predictable pattern that commercial real estate owners, including manufactured home community owner/operators, should consider when forming both short- and long-term strategic and operational business plans.

Identifying where we are in the current cycle enables us to reference past cycles for insights on expected economic policies and consumer demand going forward.

Study the Full Cycle

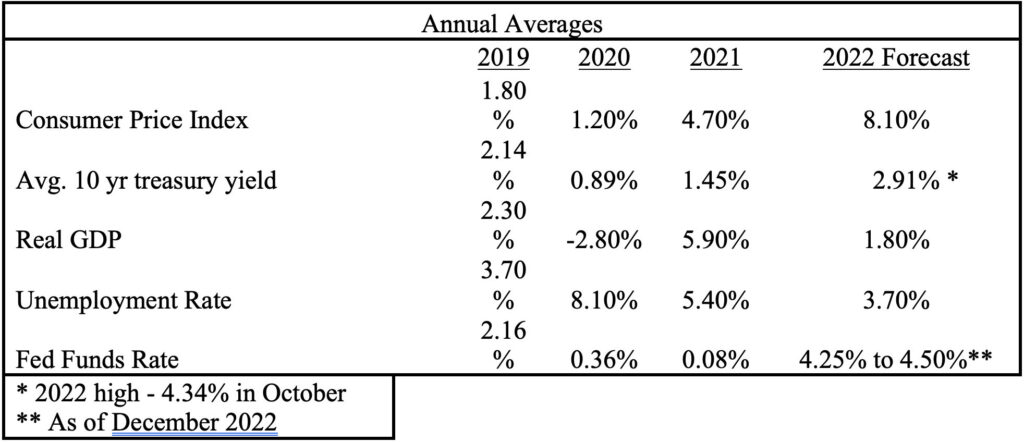

Coming out of the Great Recession of 2008, we slowly transitioned through the recovery phase, which was followed by a prolonged expansion period. In recent years, it would be reasonable to say that most markets have been in the expansion or hyper-supply phases with some markets beginning to see early signs of recession in 2022. Individual markets and property sectors often vary in terms of timing as they transition between phases with multifamily properties outperforming other sectors such as retail and office during recent market cycles. We are seeing this now with new single-family housing starts falling off faster than multifamily construction. The following chart presents key economic statistics before, during, and after the COVID-19 pandemic:

Many view the apartment sector as a relevant proxy for the MHC sector due to the extensive market data that is available. Recent surveys and reports on the apartment sector show a reversal in rent and occupancy growth during the second half 2022 as the dramatic shift in monetary policy appears to be influencing consumer behavior. Nationally, single-family units under construction declined each month in the second half of 2022. Meanwhile, multifamily new construction has continued, particularly in core markets, but the pace has slowed considerably from 2021. According to the National Association of Realtors, single-family housing starts in the third quarter of 2022 were 13% below the pre-pandemic historical average while multifamily constructed about 50% more units than the pre-pandemic average. Some experts point to prolonged construction completion delays as a reason multifamily has not slowed more, but multifamily demand is also benefiting from increases in residential mortgage rates, which have negatively impacted single-family housing affordability. Still, it is expected that rental rates will moderate in 2023, at least in some markets, given the new multifamily supply being added at a time when more people are moving back in with family or delaying moving out of their family homes, which is slowing new household formation. So, while pundits often disagree on defining what phase of the cycle we are in until after the fact, it is clear we have made a pivot.

Multiple Market Forces Impact Industry

It is also worth noting that every cycle has its unique economic and political backdrop, and our current environment has provided the Federal Reserve and policymakers plenty to consider: stubborn inflation resulting from extreme monetary and fiscal stimulus, an unusually low unemployment rate due to declining workforce participation, higher than expected consumer spending, and a war in Europe. The Fed has made it clear that it will remain steadfast in tightening monetary policy until inflation abates, even if that means overcorrection.

The continuing low unemployment rate also provides political cushion for further tightening if needed. With that in mind, while we expect the Fed will continue to raise rates in 2023, that does not necessarily mean the 10-year U.S. Treasury yield will increase in lockstep. The bond market, and particularly longer-term treasury bond buyers, respond favorably when inflation expectations are reduced. After hitting an all-time low yield of 0.52% in 2020, the 10-year U.S. Treasury yield surpassed many long-term averages when it hit 4.34% in October 2022 (its yield averaged 2.91% and 3.90% over that last 20 and 30 years, respectively).

Changes in demographics are also a factor for both policymakers and property owners to consider. One reason unemployment has remained low is because we are seeing, and will continue to see, a trend of fewer working-age Americans and more retirees. According to the Bureau of Labor Statistics, the labor force is projected to grow over the next 10 years at an average annual rate of 0.5%, which is a slower rate in comparison to recent decades. Factors include slower population growth and the aging of the U.S. population in addition to the declining labor force participation rate. In other words, finding good employees will continue to be a challenge so property owners should be prepared to budget for higher payroll expenses. Additionally, this demographic trend will have implications for required amenities and services for properties to remain competitive.

Certainly, there is a lot for property owners to consider when making business plans. From a financing perspective, we believe a case can be made that the worst of the increasing interest rate adjustment period is behind us, barring a reversal of the recent improvement in inflation measures. For property owners considering the timing and structure of their next financing, inflation will be key. While there has been much discussion about a likely recession on the horizon, it is important to remember that this is coming after a prolonged period of higher property values following the Great Recession and that periodic adjustments are healthy for the market over the long term.

About the Authors

Tony Petosa, Nick Bertino, and Matt Herskowitz are loan originators at Wells Fargo Multifamily Capital, specializing in providing financing for manufactured home communities through their direct Fannie Mae and Freddie Mac lending programs and correspondent lending relationships.If you would like to receive future newsletters from them, or a copy of their Manufactured Home Community Market Update and Financing Handbook, they can be reached at tpetosa(at)wellsfargo.com, nick.bertino(at)wellsfargo.com and matthew.herskowitz(at)wellsfargo.com.

MHInsider is the leading source of news and information for the manufactured housing industry, and is a product of MHVillage, the top marketplace to find mobile and manufactured homes for rent and sale.

{kind=link}