Investing In Manufactured Housing REITs

The research team at Hoya Capital Real Estate is excited to begin a quarterly column published in partnership with MHInsider to provide insight and commentary on publicly-traded manufactured housing stocks. Every quarter, we’ll publish an update to discuss the stock performance, earnings results, and major news and events reported by manufactured housing real estate investment trusts, or MH REITs.

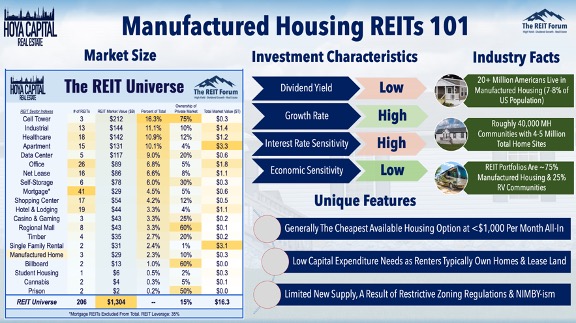

Overview of MH REITs

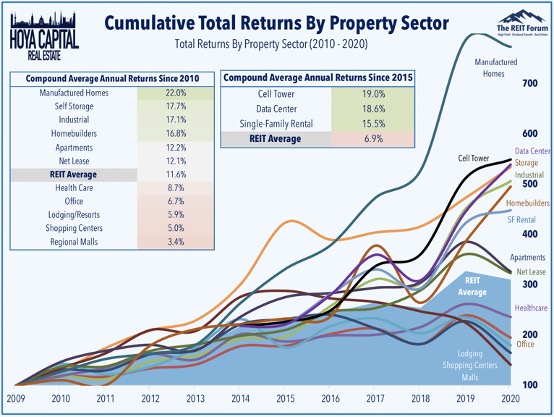

Manufactured housing REITs have been the single-best performing REIT sector since the start of 2010. Manufactured housing REITs have emerged over the past decade from relative obscurity into several of the largest publicly-traded owners of real estate in the world.

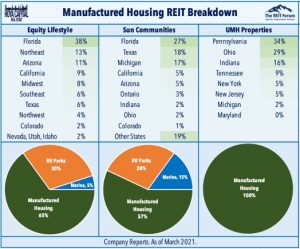

There are three publicly-traded Manufactured Housing REITs that account for roughly $30 billion in market value: Equity Lifestyle (ELS), Sun Communities (SUI), and UMH Properties (UMH).

Manufactured Housing REITs collectively own roughly 350,000 manufactured housing and RV sites across the United States with a portfolio skewed towards higher-end communities with a more “retiree-oriented” demographic than the all-ages community. Through a series of acquisitions, Equity Lifestyle and Sun Communities have recently expanded into boat marinas as well while the smaller UMH Properties has retained its “pure-play” focus on traditional manufactured housing communities.

From an investment perspective, despite their high growth rates, MH REITs are a traditionally defensive and countercyclical sector due to the “sticky” nature of MH demand and cash flows. As a result, MH REITs are less affected by economic growth expectations, but more affected by changes in long-term interest rates. While these REITs are not known for their high dividend yields, they have delivered some of the strongest rates of dividend growth of any REIT sector.

MH REITs Stock Price Performance

In the real estate sector, three themes dominated the 2010s.

- The Housing Shortage

- The Retail Apocalypse

- The Internet Revolution

No REIT sector has benefited more from the affordable housing shortage than MH REITs, which produced an incredible 22% annual compound total returns from 2010 through 2020.

Manufactured housing REITs outperformed the broad-based Equity REIT Index for a remarkable eighth-straight year in 2020, the longest streak of outperformance for any property sector since the dawn of the “Modern REIT Era” in the early 1990s.

First Quarter 2021 MH REITs Performance

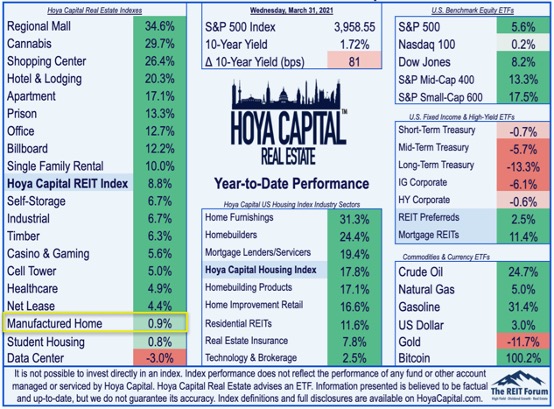

MH REITs have uncharacteristically underperformed in early 2021 even as fundamentals remain as strong as any property sector. Pressured by the post-vaccine ‘REIT Reopening Rotation’ that has sent shares of the hardest-hit pandemic-sensitive REIT sectors soaring, “essential” property sectors – housing, technology, and e-commerce – have lagged this year.

Through the first quarter of 2021, MH REITs are higher by just 1% compared to the 9% gains from the broad-based REIT Index. UMH Properties has been a winner this year, however, with gains of more than 30%.

Quarterly Earnings Report

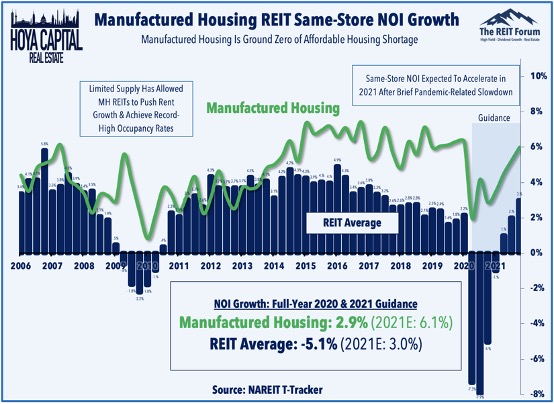

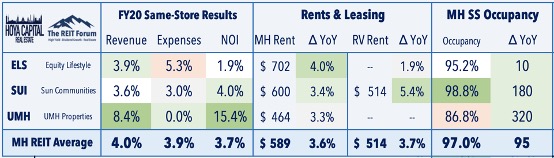

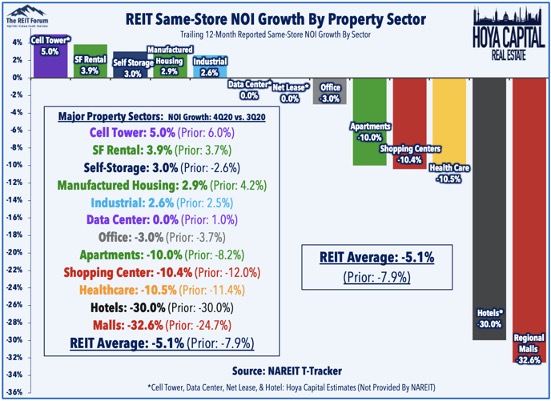

Limited supply and strong demand have driven stellar fundamental performance for MH REITs over the past decade, as these three companies have reported some of the best growth metrics of any REIT. Fourth-quarter earnings reports showed that same-store Net Operating Income (“NOI”) growth rebounded to end the year higher by roughly 3% following a pandemic-related hiccup in mid-2020. By comparison, the total equity REIT sector saw a -5.1% decline in same-store NOI in full-year 2021, the worst year on record for REITs.

The headwinds observed during the peak of the pandemic in mid-2020 – the shutdown of RV parks and the slowdown in RV and manufactured housing sales – have swiftly become tailwinds amid a broader revival across the U.S. housing industry and other WFH-related industries. The vast majority of manufactured housing residents stayed current on their rents despite rent deferment plans made available by ELS and SUI. Occupancy rates ticked higher by another 95 basis points in Q4 while “core” manufactured housing rents increased by 3.6%.

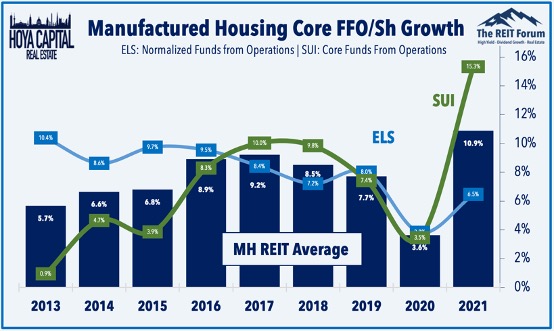

Growth in funds from operations – the earnings per share “equivalent” for REITs – is driven by the combination of same-store “organic” growth and by external growth through acquisitions and new development. Forward guidance was particularly impressive as ELS and SUI project that NOI will rise by an average of 6.1% in 2021, powering a rise in Funds From Operations (“FFO”) of more than 10% – which would likely be one of the strongest growth rates in the REIT sector.

Growth in funds from operations – the earnings per share “equivalent” for REITs – is driven by the combination of same-store “organic” growth and by external growth through acquisitions and new development.

Forward guidance was particularly impressive as ELS and SUI project that NOI will rise by an average of 6.1% in 2021, powering a rise in Funds From Operations (“FFO”) of more than 10% – which would likely be one of the strongest growth rates in the REIT sector.

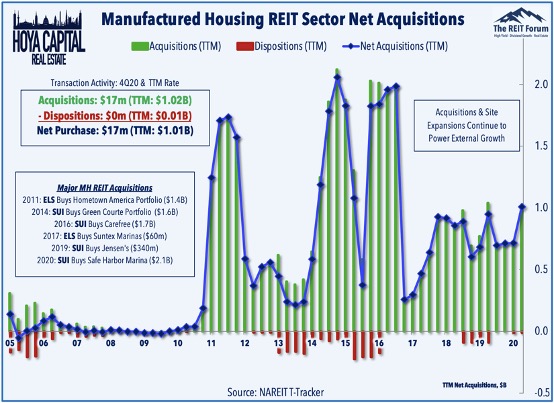

Utilizing a strong cost of equity capital, these REITs have continued to grow externally by adding units to existing sites and by growing via acquisitions and site expansions. MH REITs acquired more than $1 billion worth of properties over the last year, largely in one-off acquisitions while disposing of just $10 million in assets. The most significant deal in 2020 was Sun Communities’ $2.1B purchase of Safe Harbor Marinas, which owns and operates 101 institutional-quality boat marinas.

Average MH REIT Growth

MH REITs Net Acquisitions

MH REITs Key Takeaways

Pressured by the ‘REIT Reopening Rotation,’ MH REITs have uncharacteristically underperformed in early 2021 even as fundamentals remain strong. “Work From Anywhere” trends have powered a surge in RV, boat, and second-home sales which have provided an added external growth tailwind while same-store “organic” growth metrics remain impressive. The outlook for 2021 remains favorable with MH REITs providing guidance indicating an acceleration in earnings growth and we expect the “essential” property sectors – housing, technology, and e-commerce – to be a bright-spot again this year.

MH REITs: Terms Defined

FFO (Funds From Operations): The most commonly accepted and reported measure of REIT operating performance. Equal to a REIT’s net income, excluding gains or losses from sales of property and adding back real estate depreciation.

AFFO (Adjusted Funds From Operations): A non-standardized measurement of recurring/normalized FFO after deducting capital improvement funding and adjusting for “straight line” rents.

NOI (Net Operating Income): Typically reported on a “same-store” comparable basis, NOI is a calculation used to analyze the property-level profitability of real estate portfolios. NOI equals all revenue from the property, minus all reasonably necessary operating expenses.

Hoya Capital Disclosures

I am/we are long ELS and SUI. I am not receiving compensation for it. It is not possible to invest directly in an index. Index performance cited in this commentary does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. Nothing on this site nor any published commentary by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and should not be considered a complete discussion of all factors and risks. A complete discussion of important disclosures is available on our website www.HoyaCapital.com.

{kind=link}