Conservice, the nation’s largest utility management provider, has expanded its offerings with the acquisition of Goby and its ESG Platform to create what it believes will be a true lifecycle of products that can ease concern about field operations and inform executive boardroom decisions.

The 2021 transaction has transformed the usage data Conservice collects into a framework clients can use for environmental, social, and governance (ESG) insight and reporting tools that aid in sustainable business growth as well as regulatory compliance.

Goby has a 10-plus-year record of providing a leading data management and reporting platform.

Goby has been recognized by the EPA as a 2023 ENERGY STAR Partner of the Year, which is the 11th such consideration. The company also is a GRESB Partner, a Fitwel Champion, a ULI Strategic Partner, and a LEED Proven Provider.

“As a high-level concept, ESG refers to the sum ability of a company to operate in a way that is environmentally friendly and socially responsible,” Conservice CEO Scott Hardy said. “Naturally, utility usage is one of the key measurements that investors and governmental stakeholders use to assess an organization’s sustainability.”

Interest from all stakeholders in how a company conducts itself in regard to all of these vital areas of operation has been growing in recent years across multiple industries. The growth of the manufactured housing industry at the same time has provided opportunities for all organizations, particularly public companies, to be proactive and transparent about how they are viewed through the ESG lens.

Goby sites two fundamental steps for any organization to consider when building an ESG framework:

Measure and dashboard — the only way to scale an ESG strategy with any kind of organizational growth is to automate the process of collecting and dashboarding utility usage data

Analyze and report — most of the critical SEC requirements to emerge over the last several years have been around the need to report usage data. Being able to collate usage data into compliant reports and then analyze that data to drive business decisions is critical to getting the most out of an ESG strategy.

“Historically, any time a vertical is confronted by ESG, the companies that begin developing strategies and implementing sustainable policies early fair the best in the long run,” Conservice ESG Senior Vice President and General Manager Ryan Nelson said. “ESG continues to mature, and is relatively new in manufactured housing so now is the time for businesses in this space to engage.”

ESG stands for environmental, social, and governance, and it refers to a set of criteria used to assess the sustainability and ethical impact of a company’s operations.

Approaches to building an ESG framework in corporate settings have gained significant attention in recent years as investors, consumers, employees, and other stakeholders increasingly seek sustainable and responsible business practices.

Integrating ESG into business strategies can have several benefits, including risk mitigation, long-term value creation, improved reputation, access to capital, and resilience in the face of environmental and social challenges.

The Components of ESG

Environmental: The environmental aspect of ESG focuses on a company’s impact on the environment. It considers factors such as carbon emissions, resource usage, waste management, pollution, and climate change mitigation efforts. Companies with strong environmental practices often prioritize sustainability, energy efficiency, renewable energy, and conservation initiatives.

Social: The social aspect of ESG looks at a company’s relationships with its employees, customers, suppliers, communities, and other stakeholders. It encompasses areas such as labor rights, diversity and inclusion, human rights, employee well-being, customer satisfaction, community engagement, and philanthropy. Companies that prioritize social responsibility often foster inclusive workplaces, support fair labor practices, and contribute positively to society.

Governance: The governance aspect of ESG focuses on the internal structure and processes of a company. It includes elements such as board composition, executive compensation, transparency, accountability, risk management, and adherence to regulations and legal standards. Strong governance practices ensure that companies are well-managed, have effective oversight, and maintain high ethical standards.

What Manufactured Housing Industry Organizations Do With ESG

Various frameworks and standards exist to evaluate and report on ESG performance, such as the Global Reporting Initiative (GRI), Sustainability Accounting Standards Board (SASB), and Task Force on Climate-related Financial Disclosures (TCFD). Additionally, there are ESG rating agencies and indices that provide assessments and rankings of companies based on their ESG performance, aiding investors in their decision-making process.

It’s important to note that ESG practices can vary across industries and regions, and the specific factors considered may differ depending on the context. Nonetheless, the overarching goal is to encourage businesses to operate in a more sustainable, ethical, and responsible manner, taking into account their impact on the environment, society, and corporate governance.

we understand that delivering on our commitments to sustainability, affordability, employee empowerment, and strong and transparent governance will benefit our stakeholders,” the company’s CEO Kurt Keeney said. “At Flagship, we believe that a dedicated focus on ESG will translate into strong performance.”

The 32-page report, which can be found on Flagship’s website, includes details on water conservation and renewable energy, diversified staff and Board of Trustees, and its corporate governance structure.

At the end of last year, Flagship owned and operated 69 communities with 12,601 homesites and a portfolio-wide occupancy rate of 83 percent.

On the environmental front, Flagship has eliminated more than half the waste it was creating from the construction process for the homes they were purchasing, and a portfolio-wide community lighting program has resulted in the comprehensive use of LED lighting and solar power. It also has cut back on water consumption by more than 25 percent.

“All of these accomplishments speak to our values as an organization. Since our humble beginnings in 1995 we have always been laser-focused on doing well for investors while doing good,” Keeney said. We were pleased with our ESG performance in 2022, but we continually look to improve each year.”

In March, the third largest builder in the manufactured housing industry published its first report on ESG initiatives.

Cavco’s work affirms the company’s progress on its Corporate Responsibility Report roadmap released last year to advance its goals across the tenets of environmental stewardship, social responsibility, and corporate governance. It reports that workplace injuries from 2021 to 2022 had decreased by 18 percent even though productivity increased, including a 3.5 percent increase in hours worked. The company has reduced the cost of employee benefits by 5 percent and witnessed a 20 percent increase in health care benefit enrollment.

Wages at Cavco have increased 43.5 percent in just two years.

“The gains have been a combination of base wage increases and higher payouts through incentive programs that align pay to the success of the company,” the company stated in its report.

“Customers may not read the ESG report themselves but they’re looking for that information on the way we’re approaching things. By being more vocal about what our properties are doing, we are getting that message out.”

— Sun Communities Director of Sustainability Melissa Smith

Sun Communities may have the longest-running ESG framework in the industry.

Melissa Smith is the director of sustainability for Sun Communities and has worked on ESG efforts for 22 years.

The document evolves from year to year, as our programs and initiatives become more developed. Smith has authored three of the company’s reports and feels all stakeholders have responded positively, including residents, and RV and marina customers.

“I think people are talking about it more,” she said. “Customers may not read the ESG report themselves but they’re looking for that information on the way we’re approaching things. By being more vocal about what our properties are doing, we are getting that message out.

And while it seems the ESG framework companies endeavor in are designed for external consideration, the corporate team and the individual properties benefit from the learnings as well.

“We use them for understanding around our carbon use and greenhouse gas emissions,” Smith said.

The U.S. Securities and Exchange Commission proposed a rule last year that would require climate disclosures in financial reporting for public companies. Some private companies within a public company’s supply chain will have to report as well.

To ensure accuracy in reporting, Sun hired a pair of consultants with expertise in assisting companies to develop ESG reporting approaches.

“Because of the nuances of the industry, whether it’s manufactured housing, the outdoor portfolios, marinas, we need advice on how we would approach those properties with this element in mind,” Smith said.

Additionally, one of Sun’s largest recent acquisitions expanded its ESG interests to the UK where just this year companies are required to report on greenhouse gas and provide an interpretation of risk for climate change and how it may impact assets.

Cropped and sized image from the cover of MHInsider's July/August edition.

For a graphic designer or art director, creating an image using AI feels like it goes against the instinctual creativity and specific marketing strategy that has been engrained during an entire career. The marketing strategy, target market, creative brief, and vision that a designer typically uses to create a design or an image are of much less value in the AI platform. For an AI generator, all you really need is a handful of keywords and an art filter chosen by a drop-down menu, similar to filters used for selfies.

But this technology definitely has benefits.

I was able to generate hundreds of images of homes with futuristic, colorful, and abstract qualities. Fortunately, once an image is created it can be edited in many ways, including using the new Photoshop 2023 beta generator tool. It is a bit clunky. I’ve learned that it takes practice and knowledge of how to “interact” with AI to get the desired look. For designers looking for very specific details in their image, more research is definitely needed to work with AI, as one of the limitations is having successful strong details without disfigurement.

Most community boards and help articles basically say “keep playing around” until you get the image, and use specific, concrete words instead of abstract words. Although using abstract words can give more diversity in the images generated. Also, using words to exclude from your image is helpful to clean up the details. Some popular excluded words are blurry, disfigured, wrong, and inaccurate.

Using an AI generator to create the July/August Industry Development and Technology edition’s cover image was definitely an interesting lesson in new technology. I look forward to seeing where this technology goes!

People who apply names to things such as eras or movements may someday call early 2023 “The Spring of AI” with no small part played by the market introduction of ChatGPT, a language modeling tool from OpenAI. By the time even astute business analysts and marketing executives were aware students and teachers on a nearly global basis already were negotiating the transaction of artificial intelligence’s offerings in the classroom.

In March ask anyone in their late teens or early 20s if they’ve used Open AI’s groundbreaking offering and the answer was a wary “Oh… yeah.” It seems everyone had used it, but “not a lot”. By May all of the search engine offerings had followed Bing’s early entry into the artificial intelligence space, the breakthrough was making major magazine covers, literally, and Congressional hearings were underway.

The narrative between lawmakers and corporate heads was unlike anything seen or heard. It went something like “We know we look like magic, but we’re not, it’s a tremendous combination of science and creativity, and, quite frankly, we don’t know where it’s going. Yes, please regulate us, no not on a domestic basis, but through a global effort.”

It was as refreshing as it was bizarre.

And if some of these developments have occurred without much attention paid, the key takeaway is that the technology, the widgets it creates and the conversations around its ethical use, will impact each and every person. Not will, in fact, but is. From the CX bots to the launch of wildly sophisticated web searches you only recently have begun to see, the wave is washing over us. It is one that likely will be a boon for productivity — think of the calculator replacing the slide rule — but it’s not one that will transition into full use, whatever that is, without breaking existing architecture and creating a consumer vacuum for those who fail to plan as the waters rise.

ChatGPT itself, when asked, said “As society continues to rapidly evolve, one cannot help but wonder what lies ahead in the ever-expanding realm of technology. From groundbreaking advancements in artificial intelligence to the proliferation of smart devices, the future of technology promises to reshape our lives in profound ways.”

Language models may not be accurate in everything they convey, but ChatGPT is correct on that note.

Experts predict that AI will play an increasingly prominent role in diverse fields, including healthcare, finance, transportation, and manufacturing. The ability of machines to process vast amounts of data and make autonomous decisions is poised to revolutionize entire sectors.

The confluence of the Internet of Things (IoT), mobile and wearable smart devices, and artificial intelligence will provide vast creative solutions in nearly every realm, from the refinement of self-driving technology to smarter smart homes, from personalized remote medicine to advanced environmental practices. If AI can help improve the health and productivity of our employees in their efforts to have smarter homes self-driven to happier customers who are we to stop it?

OK, it also should be noted AI, too, writes little ditties about kitties.

So, while the future of technology presents boundless opportunities, it also raises important considerations. Ethical questions surrounding privacy, data security, and the impact on the workforce require careful examination. As technology continues to advance, society must navigate the challenge in conjunction with enjoying the voyage.

The future of technology is both awe-inspiring and transformative. We are reshaping the world in real-time.

“The path ahead may be uncertain, but the potential rewards make it an exciting time to witness,” ChatGPT said about itself.

The Federal Reserve in its July meeting opted to boost the base rates 0.25 as expected after choosing not to raise rates at the previous meeting.

Rates now stand in the 5.25 to 5.5 percent range. It’s the 11th hike in about 18 months, making for a 22-year high.

While the economy has responded positively to the recent litany of Fed moves, analysts feel the mindset is to continue moving the needle until inflation returns to 2 percent. While down from its height above 9 percent, inflation remains high at 3.6 percent, and concern persists regarding a recession later this year or early 2024.

It’s the Fed both playing it safe and being persistent. And with the July hike the FOMC likely will take a “wait and see” approach through the remainder of 2023. If it continues to view June as a turning point rates will stand, though if consumer spending continues to rise perhaps there will be one more hike in the fall.

The market impact of Fed moves remains unseen for weeks or months. The drivers that brought the economy back down to 3.6 percent inflation is based on what the Fed was doing last year, easing in the bond markets and boosting rates as high as 75 basis points at at time. So the foot is off the throttle a bit, but we probably need more pressure to land safely.

“In determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time, the committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments,” the Fed stated in a public release.

At the core of the Fed’s responsibilities lies its control over monetary policy. The Federal Open Market Committee, comprised of members from the Federal Reserve Board and regional Federal Reserve Bank presidents, determines the course of this policy. By adjusting interest rates and managing the supply of money and credit in the economy, the Fed aims to foster conditions that support maximum employment, stable prices, and moderate long-term interest rates.

East Fork Crossing is a Sun Communities property in Batavia, Ohio. Photo courtesy of Sun Communities.

Acquisition Consolidates Tech Approaches to Water Utility Efficiency

Metron-Farnier, LLC, a leader in advanced metering infrastructure, has acquired Georgia-based WaterSignal for its real-time analytics and water conservation capabilities.

The acquisition, Metron’s first since partnering with XPV Water Partners in 2019, positions the company to expand its offerings and rapidly deploy solutions in support of existing and new customers in strategic growth markets, including the real estate sector.

“As many states determine the path forward in a future with increasingly limited water supplies and failing water infrastructure, accurately monitoring and accounting for water use has become critical,” Metron CEO Matt Laird said. “Our industry-leading, high-resolution water usage analytics are helping our customers locate leaks and system failures, reduce water loss, prioritize repairs, improve revenue streams, and better manage demand.”

Laird said the Metron team is thrilled to welcome WaterSignal.

“We are motivated to achieve record results that make a significant difference for our customers. Combining our teams’ invaluable expertise and innovative technologies will allow Metron to offer expanded solutions to reach strategic markets and further improve insights and savings,” he said.

Aaron Beasley, the executive vice president of WaterSignal, said joining Metron and picking up an expanded role in serving multiple industries has been a reasonably fluid process with a team that has a reputation for listening to its customers and delivering an unmatched experience in the marketplace.

“We share many of the same values and look forward to working together,” Beasley said.

Khalil Maalouf, an investment partner with XPV Water Partners, said Metron with the WaterSignal acquisition now offers the water industry “a truly game-changing software solution” that helps customers not just track, but have a deeper understanding of water use and water use systems.

My caveats, to be clear, are that budget is not a concern, there are no approvals required, the regulatory environment will be dealt with, and hiring is the least of your worries. What’s the big idea?

The answers, of course, ran far and wide.

As I cross paths with people in the weeks and months, I will continue to add to this vault of brave notions. At some future point, MHInsider will share a good lot of them.

The concept came up during the planning and production of the State of the Industry edition of MHInsider. It looks to capture the grand themes in the industry. Rather than curating that magazine in business categories, we tackle the industry challenges and opportunities at a higher level. It’s a way to raise our considerations from the daily tactical to the long-term strategic.

We, at MHInsider, want to hear from our audience and introduce you and your ideas to the marketplace.

“What’s the Big Idea” has become my very simple big idea to help carry this bold view of how the industry might evolve through the year rather than having it designated to any two-month period. Yes, the tactical day-to-day aspects of our lives must be addressed, but not at the expense of that ringing inclination that you may have just landed on the next big idea.

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index reported a -0.5 percent annual decrease in May, down from -0.1 percent the previous month.

Chicago, Cleveland, and New York reported the highest year-over-year gains among the 20 cities in May.

At the other end of the scale, the worst performers continue to cluster near the Pacific coast, with Seattle prices down 11.3 percent, and San Francisco down 11 percent.

“The rally in U.S. home prices continued in May 2023,” S&P DJI Managing Director Craig J. Lazzara said. “Our National Composite rose by 1.2 percent in May, and now stands only 1 percent below its June 2022 peak. The 10- and 20-City Composites also rose in May, in both cases by 1.5 percent.

“Regional differences continue to be striking,” he said. “This month’s league table shows the ‘Revenge of the Rust Belt’,” Lazzara said. Chicago was up 4.6 percent, Cleveland up 3.9 percent, and New York up 3.5 percent.

S&P Dow Jones Indices provide index-based concepts, data, and research. It is the home of the S&P 500® and the Dow Jones Industrial Average®. Charles Dow invented the first index in 1884.

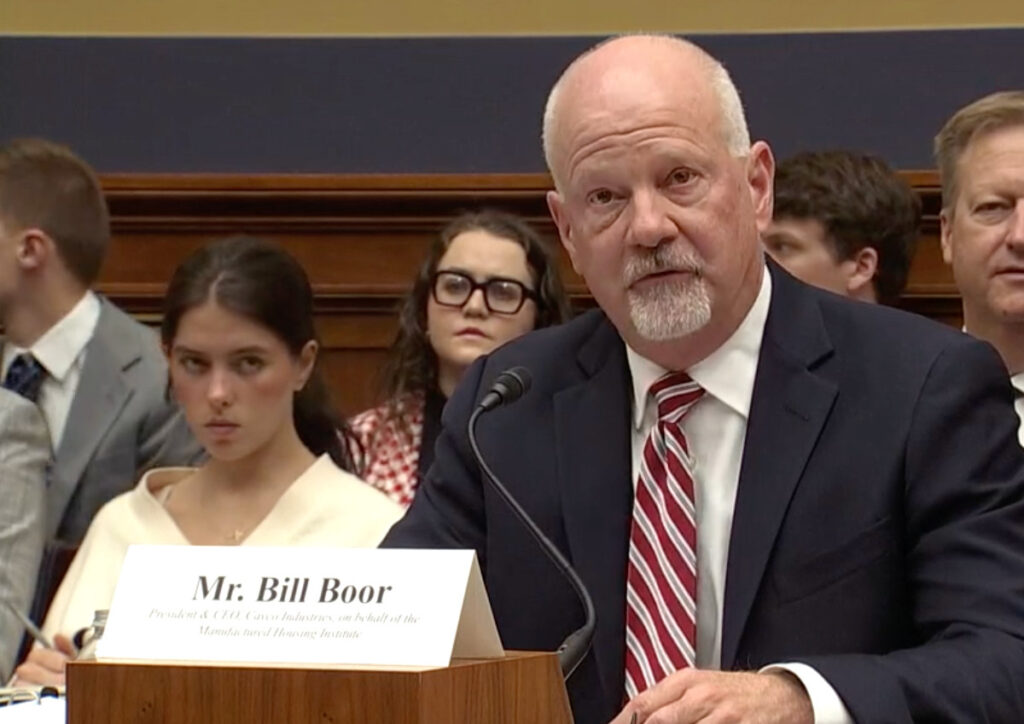

Bill Boor, the CEO of Cavco Industries, which is the nation’s third largest builder of manufactured homes, testified before the House Subcommittee on Housing and Insurance on July 14 and pointedly told members how new DOE mandates would damage the industry’s ability to build, and would keep a significant swath of potential homeowners at bay.

“Our industry has a history of significant and meaningful improvement in safety and quality. Our modern, factory-built homes compare favorably to site-built construction in durability and energy efficiency,” Boor said.

Many of the industry’s homes qualify for Energy Star certification and other government programs for energy efficiency, he said.

“In short, the subcommittee should be disavowed of any misperception that ours is a lagging industry that needs to be pulled forward with regard to ESG performance,” Boor said. “We build to a federal construction code that has been developed by and administered by HUD for 48 years and we share the objective of continually improving building standards in a balanced manner.”

“The vast majority of manufactured homes being built today exceed HUD’s standards for energy efficiency,” he said.

The subcommittee’s meeting was called to address “How Mandates Like ESG Distort Markets and Drive Up Costs for Insurance and Housing”.

Boor, who also is the vice chairman of the Manufactured Housing Institute, urged the subcommittee to consider pending legislation that would designate HUD as the industry’s lone regulatory authority, preventing DOE and other governmental bodies from making rules that unnecessarily run counter to the goal of providing affordable housing.

“DOE standards must be subject to the HUD Code process, with HUD having final authority to issue such energy standards,” Boor said. “And, HUD should follow the guidance of its experts on the subject, the MHCC – a body that has already found serious fault with the proposed DOE standards.”

Cavco, founded in 1965 in Phoenix, operate 31 manufactured housing factories across the country and has 64 retail locations, a manufactured housing lending business, and an insurance company.

“We focus on delivering the high-quality, safe, reliable, and affordable housing our customers desire in a way that benefits all of our stakeholders,” Boor told the subcommittee.

Boor said corporate responsibility is not separable from operating and growing a business, but rather is good for business and an integral component of what drives success.

“The DOE rule is a perfect example of how external ESG mandates distort markets and have unintended consequences that outweigh any potential benefit to consumers, businesses, and the environment,” he said. “The DOE rule will increase cost of manufactured homes to the point of requiring thousands of low-income consumers to remain in older, less energy-efficient housing, and miss what for many may be their only opportunity to attain homeownership.”

Manufactured housing industry professionals get a tour during the 2022 summit.

Two Days of Factory Tours, Educational Seminars for Manufactured Housing Professionals

Registration is now open for this year’s MH FacTOURy Summit, hosted at the RV/MH Hall of Fame, from Aug. 22 – 23, 2023. This event is an industry conference for manufactured housing professionals and is not open to the public.

The event will bring two days of factory tours and educational seminars to Elkhart, Ind.

Hundreds of industry professionals will have the chance to tour the region’s leading manufactured home building facilities, meet with factory representatives, see the latest manufacturing innovations, and foster new and ongoing business relationships.

“Last year’s return to Elkhart was a great success for both the MH FacTOURy Summit and the Scoular Manufactured Housing Museum, which had its grand opening last year,” Indiana Manufactured Housing Association – Recreation Vehicle Indiana Council Executive Director Ron Breymier said. “This year, we’re incredibly excited to welcome retailers, community owners, property managers, sales personnel, and other industry partners for two days of factory tours and educational seminars.”

The RV/MH Hall of Fame Induction Ceremony will precede the summit, on the evening of Monday, Aug. 21, when 10 manufactured housing and RV veterans will be honored for their industry service and enshrined in the Hall of Fame.

Special Guests to Speak at the 2023 MH FacTOURy Summit

The MH FacTOURy Summit also announced two special guests who will serve as keynote speakers for the event’s opening festivities on Tuesday, Aug. 22.

Rep. Rudy Yakym, R-Ind., will speak at the MH FacTOURy Summit on the first day of the event. Rep. Yakym is one of the co-sponsors of the Manufactured Housing Affordability & Energy Efficiency Act, a topic he will address during his speaking engagement.

Also speaking at the event is Manufactured Housing Institute Chief Executive Officer Dr. Lesli Gooch. Dr. Gooch has helped MHI become an influential and relied-upon resource for housing policy, including with Congress, the administration, the GSEs, the media and other housing industry groups. During her tenure, she has secured a number of legislative and regulatory successes and a significant increase in bipartisan support for MHI priorities.

Exhibit and Sponsorship Opportunities Available For This Year’s MH FacTOURy Summit

Exhibit and sponsorship opportunities are also open for the 2023 MH FacTOURy Summit. These are ideal ways to increase company exposure and show everything it has to offer.

Sponsors can sign up for various opportunities throughout the event to boost their brand visibility among manufactured housing professionals.

For more information regarding exhibit and sponsorship opportunities, please contact Sue Bartee at (317) 247-6258 ext. 14 or email info@imharvic.org. Visit www.mhfactourysummit.com today to register for the MH FacTOURy Summit or to learn more about the event.

More than 1,500 manufactured housing professionals are expected in Las Vegas April 7-9 as the Manufactured Housing Institute’s Congress and Expo returns to the...