The interior of a new home by Sunshine Homes, shown at the Biloxi Manufactured Housing Show in 2023.

April JLT Reports for mobile home community data in Alabama and Georgia have been published and are available for purchase, including immediate download. Datacomp is the national leader in manufactured home and mobile home valuation and community data.

JLT Market Reports provide detailed research and information on communities in 187 housing markets throughout the United States. These include the latest pricing trends and statistics, marketing programs, and a variety of other useful management insights.

Datacomp maintains and provides the JLT Market Reports and is the nation’s #1 provider of market data for the manufactured housing industry. JLT Market Reports are recognized as the industry standard for manufactured home community market analysis.

The April 2023manufactured housing market data published in JLT Market Reports for Alabama and Georgia include information from four markets on 66 “All ages” and “55+” manufactured home communities.

Altogether, the reports from Alabama and Georgia manufactured home communities include data representations for 14,180 homesites.

What’s in JLT Market Reports?

Each JLT manufactured home community report from Datacomp has detailed information about investment-grade communities in the major markets. The detailed information includes:

Number of homesites

Occupancy rates

Average community rents, and increases

Community amenities

Vacant lots

Repossessed and inventory homes, and much more

JLT Market Reports also include management insights that rank communities by the number of homesites, occupancy rates, and highest to lowest rents. Established reports show trends in each market with a comparison of April 2023 rents and occupancy rates to April 2022, as well as a historical recap of rents and occupancy from 1996 to the present date in most markets.

The April 2023 JLT Market Reports for Alabama and Georgia manufactured home communities are available for purchase and immediate download online at the Datacomp JLT Market Report website, or they may be ordered by phone in electronic or printed editions at (800) 588-5426.

Each fully updated report for mobile home communities is a comprehensive look at investment-grade properties within a market, enabling owners and managers, lenders, appraisers, brokers, and other organizations to effectively benchmark those communities and make informed business decisions.

Current Deadline of May 31 Too Early for Compliance

Builders and many other manufactured housing professionals have understood for some time that “something needs to give” in regard to the U.S. Department of Energy’s pending standards for new manufactured homes. On March 23, just weeks after the Manufactured Housing Institute and the Texas Manufactured Housing Association filed suit against the DOE, the department published to the Federal Register a request for input on a delay of compliance largely to give time for clarity on “noncompliance and enforcement”.

MHI sent a message to members encouraging them to contact the Energy Department on the matter.

“It is critical that DOE extends the compliance date for the manufactured housing energy efficiency standards until after the Department’s future enforcement procedures are created and take effect,” the message said.

The Energy Department seems to agree.

DOE has yet to issue procedures for reviewing and enforcing against noncompliance with the manufactured housing energy conservation standards, the register reads.

“A delay of the current May 31, 2023, compliance date is therefore necessary to ensure that DOE can receive and incorporate meaningful stakeholder feedback into its enforcement procedures prior to the Rule’s compliance date,” it states.

DOE stated it would expect compliance with provisions 60 and 180 days after the publication of its final enforcement procedures for Tier 1 and Tier 2 homes, respectively.

Delaying the compliance date until after the enforcement procedures are effective will provide manufacturers time to understand DOE’s enforcement procedures and prepare their operations to ensure compliance with DOE’s standards.

“…these benefits may not be fully realized if manufacturers lack clarity on how best to comply with DOE’s standards or what to expect from DOE’s enforcement of such standards,” the DOE stated.

On April 3, Sen. Tim Scott, (R), S.C., Ranking Member of the U.S. Senate Committee on Banking, Housing, and Urban Affairs, sent a letter to U.S. Department of Energy Sec. Jennifer Granholm urging her to immediately delay the new standards.

“I am concerned the DOE standards will unnecessarily limit consumer choices and raise costs for families seeking affordable homeownership opportunities,” Scott stated in his letter. “The DOE Standards are overly broad, unduly burdensome, and undermine commonsense efforts to increase supply and assist families looking for affordable housing opportunities.”

Chairman Jerome Powell explains the rationale for a 0.25 hike in interest rates during the FOMC's March meeting.

Powell Indicates Quarter Point Hike May Be Final Push

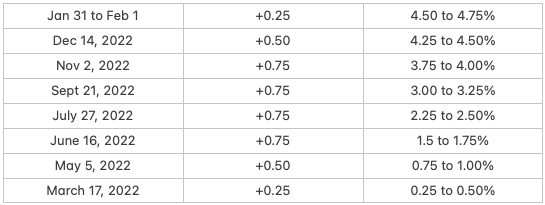

The Federal Reserve has raised interest rates by 0.25 despite recent instability in the financial sector.

Fed Chairman Jerome Powell indicated in comments following the decision to raise rates that it may be the final boost this year.

Analysts coming into the day had mixed opinions about what might happen with rates following the failure of Silicon Valley Bank, the state regulators’ seizure of Signature Bank in New York, and evidence across the sector of shaky ground for smaller to mid-size lending institutions, particularly those with ties to the tech sector.

The Fed’s move in March pushes the base rate range to 4.75% to 5%

Powell in answering questions at the meeting said there was discussion of pausing rate increases, but recent data showed that the economy is strong and the financial sector is stable. The result was the smallest possible increase to further abate inflation and hold of recession.

“Inflation pressures continue to run high. The process for getting inflation back down to 2% has a long way to go, and is like to be bumpy,” Powell said. “We understand that our actions effect communities, families, and businesses across the country.

“Everything we do is in service to our public mission,” he said. “We at the Fed will do everything we can to achieve our maximum employment and price stability goals.”

The Federal Reserve System is the central bank of the United States. It performs five general functions to promote the effective operation of the U.S. economy and, more generally, the public interest. The Federal Reserve…

conducts the nation’s monetary policy to promote maximum employment, stable prices, and moderate long-term interest rates in the U.S. economy;

promotes the stability of the financial system and seeks to minimize and contain systemic risks through active monitoring and engagement in the U.S. and abroad;

promotes the safety and soundness of individual financial institutions and monitors their impact on the financial system as a whole;

fosters payment and settlement system safety and efficiency through services to the banking industry and the U.S. government that facilitate U.S.-dollar transactions and payments; and

promotes consumer protection and community development through consumer-focused supervision and examination, research and analysis of emerging consumer issues and trends, community economic development activities, and the administration of consumer laws and regulations.

The U.S. Department of Housing and Urban Development has submitted to the Federal Register for publication a Final Rule entitled Restoring HUD’s Discriminatory Effects Standard. The Final Rule rescinds the Department’s 2020 rule governing Fair Housing Act disparate impact claims and restores the 2013 discriminatory effects rule. In the Final Rule, HUD emphasizes that the 2013 rule is more consistent with how the Fair Housing Act has been applied in the courts and in front of the agency for more than 50 years, and that it more effectively implements the broad remedial purpose of eliminating unnecessary discriminatory practices from the housing market.

“Discrimination in housing continues today and individuals, including people of color and people with disabilities, continue to be denied equal access to rental housing and homeownership,” HUD Secretary Marcia L. Fudge said. “Today’s rule brings us one step closer to ensuring fair housing is a reality for all in this country.”

The Fair Housing Act prohibits discrimination in housing and housing-related services because of race, color, religion, national origin, sex (including sexual orientation and gender identity), familial status, and disability. The discriminatory effects doctrine (which includes disparate impact and perpetuation of segregation) is a tool for addressing policies that unnecessarily cause systemic inequality in housing, regardless of whether they were adopted with discriminatory intent. It has long been used to challenge policies that unnecessarily exclude people from housing opportunities, including zoning requirements, lending and property insurance policies, and criminal records policies. Accordingly, having a workable discriminatory effects standard is vital for the Biden-Harris Administration to accomplish its goal of creating a housing market that is free from both intentional discrimination and policies and practices that have unjustified discriminatory effects.

HUD’s 2013 discriminatory effects rule codified long-standing caselaw for adjudication of Fair Housing Act cases under the discriminatory effects doctrine, for cases filed administratively with HUD and for federal court actions brought by private plaintiffs. Under the 2013 rule, the discriminatory effects framework was straightforward: a policy that had a discriminatory effect on a protected class was unlawful if it was not necessary to achieve a substantial, legitimate, nondiscriminatory interest or if a less discriminatory alternative could also serve that interest.

The 2020 rule complicated that analysis by adding new pleading requirements, new proof requirements, and new defenses, all of which made more difficult to establish that a policy violates the Fair Housing Act and harder for entities regulated by the Fair Housing Act to assess whether their policies were lawful. HUD now returns to the 2013 rule’s straightforward analysis.

This Final Rule will go into effect 30 days after it is published in the Federal Register. Due to a preliminary injunction staying the implementation of the 2020 Rule in Massachusetts Fair Housing Center v. HUD, the 2020 Rule never went into effect, and the 2013 Rule – which has been in place for nearly a decade – has been and is currently still in effect. Accordingly, regulated entities that were complying with the 2013 Rule have no need to change any practices they have in place to comply with this rule.

Timber Creek is one of several builders showing homes in Biloxi.

Miss., Ala., Show in Second Year Draws More 1,400 Professionals

The Biloxi Manufactured Housing Show and Expo at the IP Casino and Resort has staked its claim as a key industry event, drawing nearly double the number of attendees as the inaugural show in 2022. The 2023 rendition opened with a golf tournament at Shell Landing in nearby Gautier, and offered a Mardi Gras-themed opening night reception.

Tuesday was the first full day of education, exhibitor conversations, networking, and home tours.

For this year’s event, seminars and education were divided into two tracks aimed at retailers and community operators, respectively.

The event, overseen by South Central Manufactured Housing Institute comprising the Alabama Manufactured Housing Association and the Mississippi Manufactured Housing Association, runs through March 22.

Jennifer Hall is the executive director of MMHA and one of the show’s organizers.

“We surpassed 1,300 registrations, and we have more coming in. There are people who will arrive from within the state, from Alabama, and Louisiana who will register when they get to the show, so there is a lot of excitement building for this event,” Hall said. “We have 35 homes to show and I think any time you have that many new homes on site you’re going to get a lot of attention.”

Conner Mansell is the regional manager for Timber Creek Housing, a builder that began production in 2020.

“This home has a lot of flash and pop, but we manage to keep it affordable. It is a home that is very competitive for buyers who are in the site-built market,” Mansell said of The White Oak model, a 3-bedroom, 2-bath home with more than 2,200 square feet of living space. “Business is good, and traffic in Biloxi has been steady and I’m sure it will pick up as the day goes on.”

Cinnamon Woods, a UMH Properties community located in Conowingo, Md.

Datacomp, the publisher of JLT Market Reports and the nation’s #1 provider of market data for the manufactured housing industry, announces the publication of its March 2023 mobile home park comps with occupancy, home details, and other vital data on manufactured home communities from seven markets in Maryland, New Hampshire, and New York.

Recognized as the industry standard for manufactured home community market analysis for more than 20 years, JLT Market Reports provide detailed research and information on manufactured home communities located in 187 primary housing markets throughout the United States. This includes the latest trends and statistics, marketing programs, and a variety of other useful management insights.

Datacomp’s manufactured housing market data published in the March 2023 JLT Market Reports includes information on investment-grade “all ages” and “55+” manufactured home communities. Altogether, the Maryland, New York reports include data representations on 240 communities and 41,229 homesites.

What’s in JLT Market Reports?

Each JLT manufactured home community rent and occupancy report from Datacomp has detailed information about investment-grade communities in the major markets. The detailed information includes:

Number of homesites

Occupancy rates

Average community rents, and increases

Community amenities

Vacant lots

Repossessed and inventory homes, and much more

Established reports show trends in each market with a comparison of March 2023 rents and occupancy rates to March 2022. In addition, JLT Market Reports include a historical recap from 1996 to the present date in most markets.

The March 2023 JLT Market Reports for seven markets in Maryland, New Hamphire, and New York are available for purchase and immediate download online at the Datacomp JLT Market Reports, or they may be ordered by phone in electronic or printed editions at (800) 588-5426.

Each fully updated report for mobile home communities is a comprehensive look at investment-grade properties within a market, enabling owners and managers, lenders, appraisers, brokers and other organizations to effectively benchmark those communities and make informed decisions.

U.S. Department of Housing and Urban Development will host the 2023 Innovative Housing Showcase on the National Mall from June 9-11.

The Showcase is a public event to raise awareness of innovative and affordable housing designs and technologies that have the potential to increase housing supply, lower the cost of construction, increase energy efficiency and resilience, and reduce housing expenses for owners and renters.

“The Innovative Housing Showcase is an excellent opportunity for HUD to exhibit the creative approaches industry leaders across the country are taking to the building, design, and development of our nation’s housing,” said HUD Secretary Marcia L. Fudge. “I invite everyone to join us on the National Mall this June to see our collaborators’ ingenuity on full display.”

More than 2,500 people — including policymakers, housing industry representatives, media, and the general public — are expected to attend. There will be more than a dozen exhibits, including full-sized prototype homes that represent the future of housing.

This will be the third time HUD has hosted the event, the first time in 2019, and in June of 2022. The event is timed with National Homeownership Month. Each year the lineup of homes has included manufactured homes and modular homes.

Industry Learning, Networking with MHI

The Manufactured Housing Institute in previous years has scheduled in coordination with IHS its industry fly-in day and the Homes on the Hill event that provides an invitation to legislators, staff, and policymakers for a hosted walk-through of the homes. The 2023 Homes on the Hill will be held June 6-7, just prior to the HUD event.

MHI will have an opening night reception at the host hotel, which will be announced in the weeks to come. Members will meet for breakfast the following morning, and receive an industry briefing. Industry representatives will take the day to talk with lawmakers and staff about priorities, challenges, and opportunities before coming back down to the National Mall for a mixer, and a tour of the homes.

Federal Reserve Chairman Jerome Powell giving a statement Feb. 1, 2023.

In early March analysts held the expectation of the Federal Reserve instituting a second rate hike of a quarter point, but a week marked by a stronger jobs report than anticipated and the failure of Silicon Valley Bank has most market watchers scratching their heads.

Total non-farm payroll employment rose by 311,000 in February, and the unemployment rate edged up to 3.6%, the U.S. Bureau of Labor Statistics reported on March 10.

The first glance at 86,000 more jobs than anticipated might point to the 0.50% increase, but the closer look at the jobs report showed growth in key sectors in need of employment and a lull in sectors that were do some right sizing.

Notable job gains occurred in leisure and hospitality, retail trade, government, and health care. Employment declined in information, and in transportation and warehousing.

“This jobs report managed a neat trick: Good news for both workers and the Fed,” Navy Federal Credit Union Economist Robert Frick was quoted as saying by Forbes. ”For workers, hiring continues to be robust, especially in industries that need people most: leisure and hospitality, retail, government and healthcare… That may blunt the Fed’s ardor for raising rates much more.”

The bank run in Silicon Valley added to that probability.

Silicon Valley Bank Failure Being Sorted Out, New York Institution Added to the List

The SVB failure has caused concern well beyond Menlo Park, Calif. The thought that other financial institutions could be at risk was accentuated March 13 with the regulatory shutdown of Signature Bank in New York. While the SVB loss has been characterized as “idiosyncratic” because of the nature of the bank — a majority of accounts held by large depositors — measures are being taken to achieve the needed stability for all institutions.

While the FDIC insures most U.S. deposits up to $250,000, that does little for accounts at an institution like SVB where customers are legacy clients fro the tech industry with holdings larger than the insured amount. A run on the bank ensued, and the institution cashed in bonds to pay out the withdrawals, which sent more customers asking for their cash.

Regulators are working to ensure solvency, through a sale or other means. President Biden has echoed industry regulators’ insistence that the problem will be resolved without depositors losing money.

As part of the security net, the Fed has stated it will allow banks that are well-collateralized with government guarantees access to loans that will help pay out any short runs on deposits, which would save the marketplace from a glut of sell-offs similar to the one that sent SVB into a spiral.

Fed Rate Hikes in 2022-23

Analysts began the month believing the Fed may raise rates again by 0.25 basis points, then sentiment leaned toward a half point. Only midway through March, there is speculation the Fed may stay put.

“The board is carefully monitoring developments in financial markets,” the Fed stated in its March 12 release. “The capital and liquidity positions of the U.S. banking system are strong and the U.S. financial system is resilient.”

Silicon Valley Bank, which still held more than $200 billion in deposits, represents the second-largest U.S. bank failure in U.S. history, behind only to Washington Mutual’s $307 billion collapse in 2008.

Third on that list now is Signature Bank with a $118 billion collapse.

State regulators stepped in on Signature Bank, a large lender in the crypto space, to avoid a run-off on the heels of indications that the institution was unable to prove its ability to maintain stability in the case of higher-than-usual withdrawals.

Leadership at both banks will be replaced by third-party administrators who will pore over the books and look to correct course.

The labor force participation rate was little changed at 62.5%, and the employment-population ratio held at 60.2%. These measures also have shown little net change since early 2022, and remain below their pre-pandemic levels.

The strong report gives some analysts and market watchers pause on what may have been an expectation for moderation in rate hikes when the Federal Reserve meets again in late March. After consecutive half- to three-quarter point increases through 2022, the Fed started the year with a 0.25 increase and was expected by many to hold that pattern.

Analysts agreed that the robust job report may be a signal to the Fed that its heavy push is not yet complete, but that was prior to news on the two failed banks.

The goal for the Fed is to alleviate inflation, which peaked last year near 9% and remains above 6%. The standard is for inflation to sit at about 2% to achieve market-wide price stability, for consumers and investors.

The Fed is scheduled to meet again on March 21-22.

California Attorney General Rob Bonta at a recent press conference.

Huntington Beach Accused of Targeting Affordable Housing Protected by State

Gov. Gavin Newsom, Attorney General Rob Bonta, and the California Department of Housing and Community Development filed suit and a motion for a preliminary injunction against the City of Huntington Beach alleging violations of state housing law.

The suit comes after the Newsom administration and Attorney General Bonta urged the municipality through separate enforcement authorities to reject unlawful and willful attempts to “flout state housing law”.

In a statement issued with the filing, the California offices said Huntington Beach’s actions directly threaten statewide efforts to increase the availability of low- to middle-income housing opportunities in the midst of a statewide housing crisis.

“My administration will take every measure necessary to hold communities accountable for their failure to build their fair share of housing,” Gov. Newsom said. “The housing crisis facing families across the state demands that all cities and counties do their part, and those that flagrantly violate state housing laws will be held to account.”

Where Local Governments Oppose

On March 7, the Huntington Beach City Council declined to reverse its Feb. 21 action banning the processing of applications for Senate Bill 9 (SB 9) projects and accessory dwelling units (ADUs) projects.

The state contends the municipality is in violation of multiple state housing laws. The city also introduced, but has not yet adopted, an ordinance purporting to exempt itself from the “Builder’s Remedy” provision of the California Housing Accountability Act that aims to streamline approval of affordable housing projects in cities that do not have what is known as a “compliant housing element”.

Huntington Beach is required by the state to plan for 13,368 new housing units over the next eight years.

“As our state faces an existential housing crisis, we won’t stand idly by as local governments knowingly flout state law meant to protect our communities and bring much needed affordable housing to the people of California,” California Attorney General Bonta said. “Huntington Beach’s latest moves fly in the face of the law, stifle affordable housing projects, and infringe on the rights of private property owners in their own community.

California on Housing Affordability

The suit seeks to hold Huntington Beach accountable for its leadership’s knowledge of and disregard for state housing law and put a stop to unlawful attempts to obstruct crucial projects.

“I’ve said it before and I’ll say it again: When it comes to building affordable housing, we all have a part to play, and Huntington Beach is no exception,” Bonta said.

In the complaint, the state argues that the ban on the approval of certain affordable housing projects is illegal and must be struck down.

The combined statement said California leadership stands united in commitment to defense of and increasing access to affordable housing. In 2021, Governor Newsom launched a Housing Accountability Unit increasing stringent enforcement and oversight at the local level to create more housing, faster across California.

Tucson Estates, a residential neighborhood west of Tucson, Ariz.

PorchPass™ is a new product that was developed and launched by Braustin Homes to bring a speedy financial technology offering for homebuyers interested in a manufactured home on land.

The company said the new product, available online, streamlines the manufactured home construction process, giving buyers the power and speed of a cash close.

“It’s hard to compete with cash buyers,” Braustin Homes CEO Alberto Piña said. “PorchPass will expand the pie by helping the industry say yes to more customers looking for homes in the $250,000 range. No one else is providing this kind of solution in the $20B+ factory-built home market.”

Nearly a third of manufactured home customers who have already been approved for a mortgage also need a land-home construction loan, which sometimes is challenging to navigate. These often-complicated loans, with high rates and fees, can take up to 140 days to clear, putting potential homeowners at risk of losing their dream property to a cash buyer.

PorchPass has secured the financial backing to streamline the process, giving prospective homeowners the same leverage as cash, with the ability to pay the land seller in 14 days, and save up to $15,000 or more in construction loan bank fees.

“Fintech harnesses the power of technology to make something old school simpler and more accessible for more people,” said Rackspace Technology Co-Founder Pat Condon, who serves on the Braustin Homes board of directors. “PorchPass’s fintech platform streamlines the traditional process for obtaining a construction loan, utilizing desktop appraisals, online applications, and other virtual tools that help buyers skip many of the expensive, time-consuming steps that put their land acquisition at risk.”

Competitive Market Calls for More Affordable Options

According to data reported by the Case-Shiller Home Price Index, an average single-family house in the United States costs nearly eight times the U.S. median annual household income. A new White House plan for boosting affordable housing calls for reviving the production of factory-built homes , which are increasingly more customizable and appointed with high-end features that make them a desirable option in the mainstream residential market.

Now that the supply chain is improving, and manufacturers have lifted their allocation limits on how many homes each dealer can sell, Braustin Homes is launching the new fintech platform in Texas, which accounts for approximately 20% of the national manufactured homes dealership market.

PorchPass was initially available to Braustin customers and is now offered to select dealerships in a pilot program.

“The speed of PorchPass will make more affordable mortgage products, including FHA and VA home loans, available to people in the manufactured housing space,” Braustin Homes Chief Financial Officer Edward Stepanow said. “Most land sellers won’t wait four months for an FHA loan to process in this hyper-competitive market. Now, more people will be able to compete with cash buyers and other faster financing.”

How PorchPass works:

PorchPass validates that a buyer has been approved for a legitimate, underwritten mortgage.

PorchPass steps in as a cash buyer, using cash to lock down the land, the home, and the contractor services so that a single-family residence can be built in 60 to 90 days.

PorchPass then assembles all three components into a mortgage-ready product, which is sold to the homeowner, who purchases it with their pre-approved mortgage (mortgage companies cannot finance these three pieces individually).

“You can’t have a truly virtual way to buy a home without a virtual way to streamline the financial process,” says Piña. “PorchPass brings our virtual offerings full circle.”

In August, the RV/MH Hall of Fame will celebrate the 2025 class of inductees, five from each industry.

“Our selection committees held meetings to review...